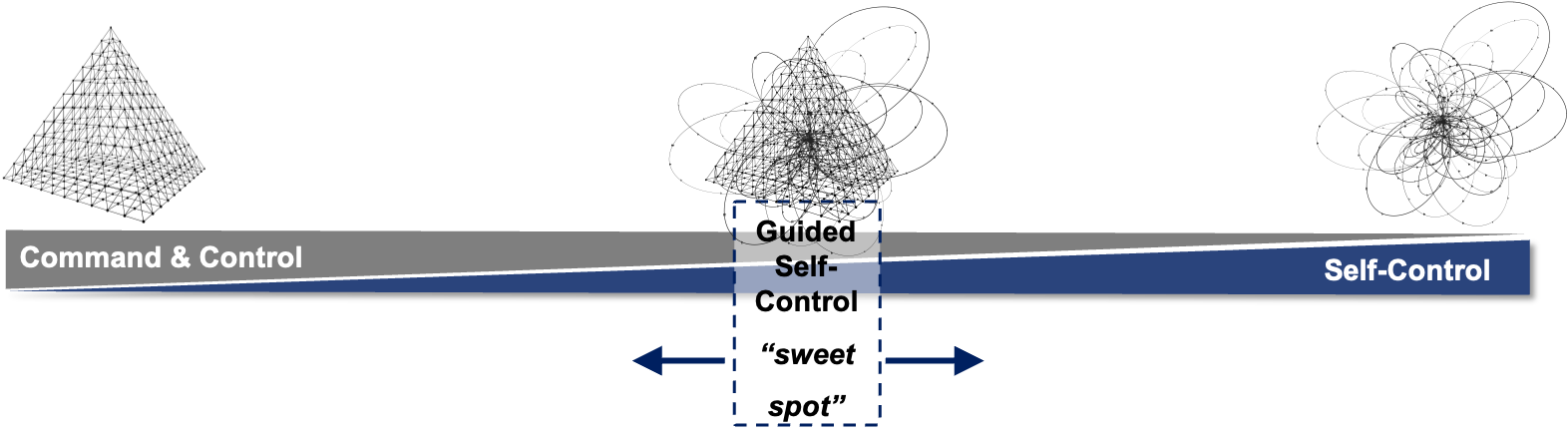

Guided Self-Control

In order to ensure a sustainable change in a company's management and control system and to effectively replace the "Command & Control" pattern, systematic support for self-control through the adaptation of practices at the organizational, team and individual level is required.

From our practical experience, the following five building blocks for guided self-control have proven to be effective and helpful.

Forecast

Planning

from action planning

and relative performance measurement

with rolling forecasts

North-Star targets

rolling planning and OKRs

North Star

Targets

Priorities

Initiatives

Control

Function/

Team - Level

By making tailored adjustments to the management system, it is possible to increase the degree of self-control and consequently the company's adaptability without completely restructuring the organization.

It is crucial to find the right area for the organization between tight controls ("Command & Control") and a high degree of autonomy, which we call the sweet spot . This optimal “mixing ratio” creates an optimal impact and is dependent on both the dynamics of the market environment and the structure of the business model.

A first important conceptual step to break up the “Command & Control” control pattern is to separate the financial target setting - the motivation function of a budget - from the planning of resources and actions to achieve the objectives >em>- the coordination function of a budget.

In the traditional management system financial targets are combined with initiatives and tasks, which lead to one total plan for the organization, the operating plan, business plan, or in general the budget. This budget merges the target and the way how to get there to an identity and documents as consistently as possible across all functions (horizontally) and levels (vertically) what (= financially) the target is and how (= with which means) is to be achieved. It is implied that it is possible to plan and describe exactly what the path to the target looks like. With today's market dynamics, however, this guideline for decisions and actions is an illusion and cannot be provided by an overall plan or fixed budget and could lead to serious misallocations.

This design flaw is deliberately corrected here. Financial targets should provide orientation and direction in the sense of a “North Star” (see module # 2). The planning and coordination of actions takes place in a decentralized, self-controlled process in which progress is regularly measured and resources are coordinated on the basis of a realistic forecast.

The creation of detailed, annual budget targets in a dynamic and complex (VUCA) environment is not only a waste of time, but they also convey a false sense of security and are a poor benchmark for measuring performance.

Viel effektiver und aussagekräftiger sind relative strategische Ziele für einige wichtige Leistungstreiber der finanziellen Wertschöpfung des Geschäftsmodells des Unternehmens. Das von uns als „House of Performance“ bezeichnete Zielgerüst fokussiert dabei auf die drei Werttreiberdimensionen: Wachstum, Profitabilität Kapitaleffizienz und wird sowohl für die Steuerung von Profit-Centern (z.B. Vertriebsgesellschaften, Business Units) als auch für die Steuerung von als Service und Cost Center geführten Organisationseinheiten (z.B. Werke und Logistikfunktion und sonstige Support-funktionen) angewendet. Die Ziele sollen möglichst relativ selbst-adjustierend gestaltet und von der Strategie abgeleitet sein, damit sie auch im dynamischen Umfeld eine Orientierung im Sinne eines “Nordsterns” geben können.

Self-adjustment occurs when the target (and thus also a target amount) automatically adapts itself due to the change in a reference value on the basis of a target function (rule-based) without the intervention of the actors involved (e.g. management).

Example: Target sales growth 1.5 times as much as the market (reference value); sales in t0 = 100; in t1 the market grew by 6% -> target 1.5 * 6% = 9% -> target amount for t1 = 109.

In a target system with relative North Star targets, the reference points of the performance measurement change dramatically. The progress, i.e. closing the gap to the strategic North Star targets becomes the central benchmark for the performance assessment. Performance measurement moves away from plan-to-actual and focuses on trends and actual-to-actual comparisons. Rolling averages or sums over different periods of time, e.g. 4 or 12 months, are used. Planning figures become completely obsolete. By doing this developments and trends can be tracked over longer periods of time. By observing longer time series with a rolling period reference, one breaks away from the rigid, fiscal year-oriented annual reference and thus gains a better understanding of developments.

Targets that are designed relative to the market (competitors / peers = external reference, e.g. benchmark - especially in areas close to the market -) increase the informative value, as they can measure and assess the own performance of the organization in a market related manner from an external perspective.

Both the orientation towards progress in reaching the strategic Nord Star targets, as well as the continuous measurement of trends and developments lead to a significantly higher level of transparency and understanding of the company's performance compared to plan-actual comparisons with an outdated budget.

Ein typisches Element von «Command&Control» basierten Steuerungssystemen ist das Setzen von Motivationsanreizen mit variablen Vergütungsmodellen, die an die individuelle Zielerreichung gekoppelt sind. Dieser „pay for (individual) performance“ Ansatz ist in der Praxis immer noch weit verbreitet, obwohl es seit Jahrzehnten wissenschaftliche Belege dafür gibt, dass dieser Ansatz insbesondere bei komplexen Arbeitsinhalten sogar leistungsmindernd wirken kann.

Die Vereinbarung von Zielen ist weiterhin unverzichtbare Basis konstruktiver Zusammenarbeit. Sie muss auf hohem Niveau und mit hoher Verbindlichkeit stattfinden. Auch die Kopplung des Einkommens an den Erfolg des Unternehmens ist gerade bei hoher Dynamik sinnvoll. Dies kann sehr effektiv erreicht werden, indem variable Vergütungselemente mit dem Fortschritt der gesamten Organisation in Richtung des längerfristigen relativen Nordstern-Ziels verknüpft werden. Dadurch entsteht ein Erfolgsbeteiligungsmodell mit perfekter Synergie zu den Bausteinen #1 und #2.

Building Block #4: Define and execute strategy with rolling planning and OKRs

The entire organization is now aligned with the relative, self-adjusting target system in order to achieve the strategic goals of the organization. There is no longer any need for energy-sapping annual target setting exercises. The focus and energy of an organization can be put on planning and executing strategic initiatives and activities. The separation from financial targets opens up much more space for continuous and self-organized planning processes.

Dieser Kontext eignet sich perfekt für die Anwendung eines agilen Führungsmodells wie OKRs (Objectives and Key Results).

Dabei werden auf Basis der strategischen Ziele der Organisation ambitionierte Ziele für Organisationseinheiten und Teams (Objectives) mittels Beteiligung der jeweiligen Mitarbeiter formuliert und zu diesen jeweils mess- und beurteilbare Schlüsselergebnisse (Key Results) definiert. Die OKRs werden dann in festgelegten unterjährigen Zyklen überprüft/reflektiert und aktualisiert.

Durch das Zusammenspiel des dynamischen OKR Ansatzes mit dem Nordstern-Zielsystem wird Strategieumsetzung zu einem rollierenden, selbstgesteuerten Prozess, der sowohl Stabilität in der strategischen Orientierung als auch Agilität bei der Anpassung der Massnahmen optimal verbindet.

Building Block #5: Add greater flexibility to resource allocation with rolling forecasts

A very lean rolling forecast (RF) process forms the fifth building block towards guided self-control. The RF ensures a coordinated process for checking and adjusting the resource allocation. As a rule, this takes place for a period of 12 months in a 3 to 4-month rhythm that is synchronized with the rolling planning process (building block # 4) and meets the requirements of a more complex and dynamic business environment.

Ein sehr wichtiges Merkmal des RF ist, dass er keine Ziel- / Motivationsfunktion hat. Diese wird bereits vom relativen Nordstern-Zielsystem abgedeckt. Der RF ist dadurch nicht mehr die Basis für das nächste Budget und somit systematisch von taktischen Überlegungen befreit. Er fungiert als reine Prognose und als «Taktgeber» für die Überprüfung von Ressourcenallokationsentscheidungen.